- Published on

- Veemi Accounting

What Is Payroll Reconciliation and Why Does It Matter for US Businesses?

For many US businesses, payroll is one of the largest recurring expenses, and one of the easiest places for costly mistakes to occur. A simple payroll error, whether it’s an incorrect tax withholding, duplicate payment, or missed overtime calculation, can quickly lead to IRS penalties, employee dissatisfaction, and inaccurate financial reporting.

Yet despite its importance, many businesses only discover payroll discrepancies during tax season or after an employee raises a concern. By then, correcting the issue often requires significant time, effort, and additional costs.

This is where payroll reconciliation becomes essential.

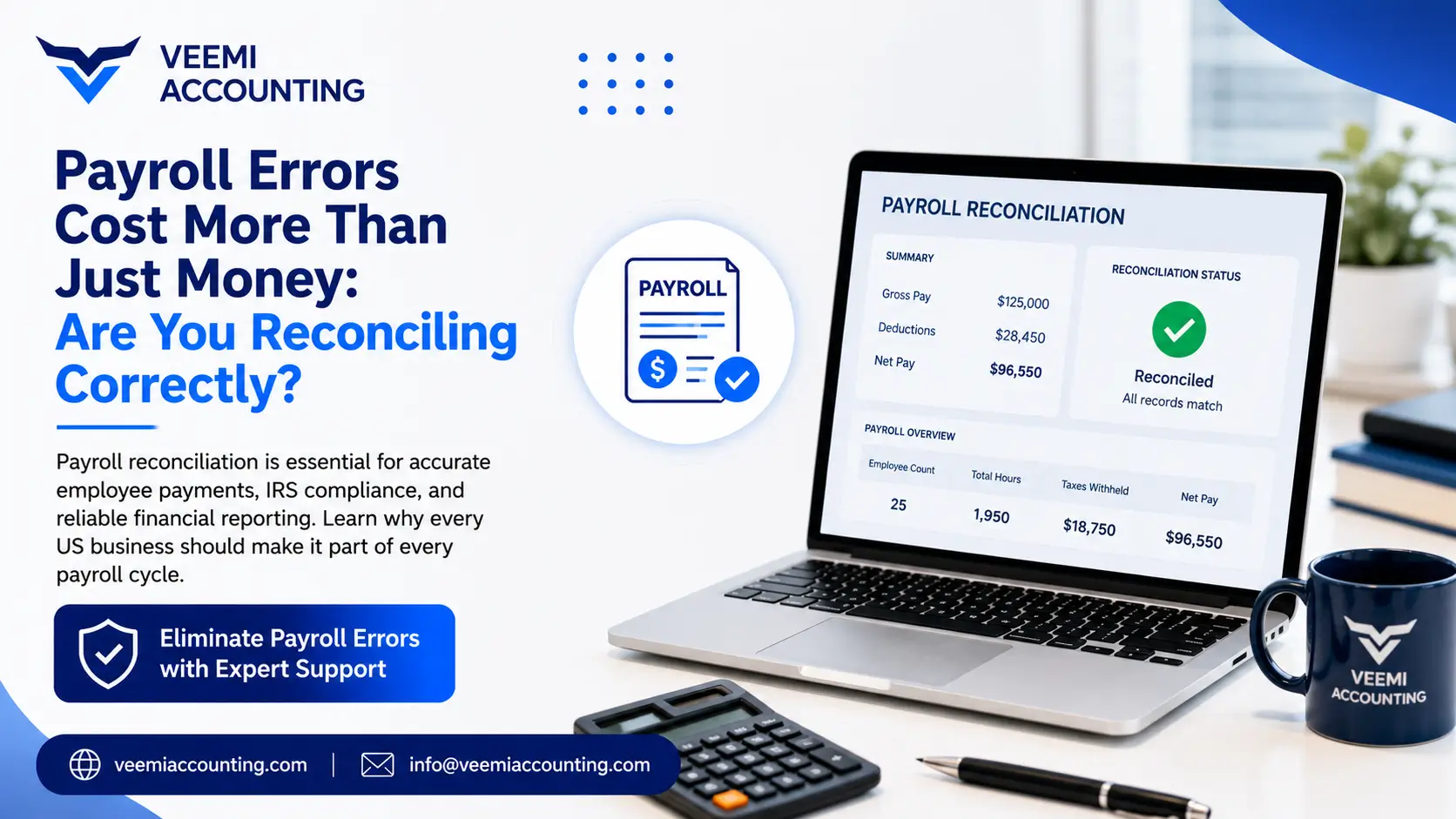

Payroll reconciliation is the process of verifying that payroll records match accounting records, bank transactions, and tax filings. It helps ensure employees are paid accurately, taxes are calculated correctly, and financial statements remain reliable.

In this guide, we will explain what payroll reconciliation is, why it’s critical for US businesses, how the process works, common mistakes to avoid, and why many companies are outsourcing payroll reconciliation to experienced accounting professionals.

What Is Payroll Reconciliation?

Payroll reconciliation is the process of comparing payroll records with other financial records to ensure every payroll transaction has been recorded accurately and completely.

Rather than simply processing employee salaries, reconciliation confirms that the numbers flowing through payroll align with:

👉 Payroll registers

👉 General ledger (GL)

👉 Bank statements

👉 Payroll clearing accounts

👉 Federal payroll tax filings

👉 State payroll tax filings

👉 Employee benefit deductions

👉 Employer tax obligations

The objective is to identify and resolve discrepancies before they become larger financial or compliance issues.

What Gets Reconciled?

A thorough payroll reconciliation typically includes verifying:

👉 Gross wages

👉 Regular and overtime pay

👉 Bonuses and commissions

👉 Federal income tax withholding

👉 State and local tax withholding

👉 Social Security and Medicare taxes

👉 Employer payroll taxes

👉 Retirement contributions

👉 Health insurance deductions

👉 Garnishments

👉 Paid leave balances

👉 Payroll liabilities

👉 Net employee payments

Every figure should reconcile across payroll software, accounting records, and actual bank transactions.

Payroll Reconciliation vs. General Bookkeeping Reconciliation

Although both processes focus on accuracy, they serve different purposes.

General bookkeeping reconciliation ensures that bank accounts, credit cards, and accounting records match.

Payroll reconciliation, however, focuses specifically on employee compensation, payroll taxes, deductions, and employer obligations.

Payroll reconciliation also requires compliance with federal, state, and local payroll regulations, making it significantly more specialized than standard bookkeeping reconciliations.

Why Payroll Reconciliation Matters for US Businesses

Payroll reconciliation is far more than an accounting task; it protects the financial health and legal compliance of your business.

Ensures IRS and State Compliance

Employers must accurately report payroll taxes through filings such as:

👉 Form 941 (Quarterly Federal Tax Return)

👉 Form 940 (Federal Unemployment Tax)

👉 State unemployment filings

👉 State income tax filings

👉 Local payroll taxes are applicable

Reconciling payroll before filing these returns helps identify reporting errors before they trigger notices or audits.

Payroll reconciliation directly impacts the accuracy of your financial statements, budgeting, and business decisions. Learn more about how reliable financial reporting supports long-term growth in our guide on Why Financial Reporting Matters More Than Just Filing Taxes.

Prevents Costly Payroll Tax Penalties

Payroll tax mistakes are among the most expensive compliance errors businesses make.

Incorrect payroll reconciliation may result in:

👉 Underpaid payroll taxes

👉 Overpaid payroll taxes

👉 Incorrect employee withholdings

👉 Missed payroll deposits

👉 Late tax filings

These errors can lead to penalties, interest charges, and additional administrative work.

Detects Payroll Errors Early

Regular reconciliation helps uncover issues such as:

👉 Duplicate employee payments

👉 Incorrect pay rates

👉 Ghost employees

👉 Missed overtime

👉 Incorrect benefit deductions

👉 Payroll software setup errors

👉 Manual data entry mistakes

Finding these discrepancies early prevents them from snowballing into larger financial problems.

Improves Financial Reporting

Payroll is a significant operating expense.

If payroll records are inaccurate, businesses may experience:

👉 Incorrect profit calculations

👉 Distorted operating expenses

👉 Poor budgeting decisions

👉 Misleading financial statements

👉 Cash flow forecasting issues

Payroll reconciliation ensures accounting records reflect actual payroll costs.

How Payroll Reconciliation Works (Step-by-Step)

A structured payroll reconciliation process helps businesses maintain accurate financial records while reducing compliance risks.

Step 1: Gather Payroll Records

Collect all relevant documentation, including:

👉 Payroll register

👉 Employee earnings reports

👉 General ledger

👉 Bank statements

👉 Payroll tax reports

👉 Benefit reports

👉 Payroll clearing account records

Having complete records makes reconciliation more efficient and accurate.

Step 2: Compare Payroll Reports

Verify that payroll software reports match:

👉 Gross payroll

👉 Employee deductions

👉 Employer contributions

👉 Payroll taxes

👉 Net pay

Any discrepancies should be investigated immediately.

Step 3: Verify Payroll Tax Liabilities

Confirm that payroll taxes have been calculated correctly, including:

👉 Federal withholding

👉 Social Security

👉 Medicare

👉 Federal unemployment taxes

👉 State payroll taxes

👉 Local taxes

Also, verify employer contributions for benefits and retirement plans.

Step 4: Match Payroll to Bank Transactions

Review payroll bank withdrawals to ensure they align with:

👉 Employee direct deposits

👉 Payroll tax payments

👉 Benefit provider payments

👉 Payroll clearing account balances

Unexpected withdrawals or unmatched transactions require further investigation.

Step 5: Resolve Discrepancies

If differences are identified:

👉 Review employee records

👉 Check payroll settings

👉 Correct journal entries

👉 Update payroll software

👉 Process payroll adjustments if necessary

Timely corrections prevent errors from carrying into future pay periods.

Common Payroll Reconciliation Errors US Businesses Face

Even businesses using modern payroll software can encounter reconciliation issues.

Employee Misclassification

One of the most common payroll mistakes is classifying workers incorrectly.

Examples include:

👉 Independent contractors treated as employees

👉 Employees incorrectly paid as contractors

👉 Incorrect W-2 or 1099 reporting

These mistakes can create significant tax liabilities.

Incorrect State Tax Withholding

Businesses operating in multiple states often face payroll tax complexity.

Common issues include:

👉 Wrong withholding rates

👉 Incorrect state unemployment calculations

👉 Missing reciprocal state agreements

👉 Local tax calculation errors

Manual Data Entry Errors

Companies using spreadsheets or multiple systems often encounter:

👉 Duplicate entries

👉 Missing payroll journals

👉 Incorrect employee information

👉 Transposed numbers

Automation reduces, but does not eliminate, these risks.

Missed Overtime or Benefit Deductions

Incorrect payroll calculations may result from:

👉 Overtime not being applied

👉 Missing health insurance deductions

👉 Retirement contribution errors

👉 Incorrect paid leave calculations

Regular reconciliation catches these issues before they become recurring problems.

Consequences of Skipping or Delaying Payroll Reconciliation

Ignoring payroll reconciliation can create serious financial and operational risks.

IRS Penalties and Interest

Payroll tax inaccuracies can trigger:

👉 Late payment penalties

👉 Interest charges

👉 IRS notices

👉 Payroll tax audits

These costs can quickly exceed the effort required for regular reconciliation.

State Compliance Risks

For businesses with employees in multiple states, reconciliation helps ensure compliance with varying state tax requirements.

Without it, companies may face:

👉 State audits

👉 Penalties

👉 Additional reporting requirements

👉 Delayed tax filings

Inaccurate Financial Reporting

Unreconciled payroll affects:

👉 Profit and loss statements

👉 Balance sheets

👉 Cash flow reports

👉 Budget forecasts

Poor financial data can lead to ineffective business decisions.

Employee Dissatisfaction

Payroll errors often result in:

👉 Late payments

👉 Incorrect deductions

👉 Delayed reimbursements

👉 Payroll disputes

These issues can damage employee morale and increase turnover.

Why US Businesses Are Outsourcing Payroll Reconciliation

As payroll regulations become more complex, many businesses are choosing to outsource payroll reconciliation instead of managing it internally.

Here’s why:

Reduced Administrative Burden

Outsourcing allows business owners and finance teams to focus on strategic priorities instead of spending hours reconciling payroll records.

Access to Payroll Compliance Expertise

Experienced accounting professionals stay current with:

👉 Federal payroll tax regulations

👉 Multi-state payroll requirements

👉 Tax filing deadlines

👉 Payroll reporting changes

This expertise helps reduce compliance risks.

Lower Costs

Hiring, training, and retaining payroll specialists can be expensive.

Outsourcing often provides access to experienced professionals at a lower overall cost while improving accuracy and efficiency.

For CPA firms managing multiple clients, outsourcing payroll reconciliation also increases operational capacity and helps maintain consistent service quality.

Many growing businesses are outsourcing payroll reconciliation alongside bookkeeping and accounting to improve accuracy, reduce compliance risks, and lower operating costs. Discover why more companies are making the shift in our article Why US Businesses Are Moving to Outsourced Accounting in 2026.

Turn Payroll Accuracy Into a Competitive Advantage

Payroll reconciliation isn’t just another accounting task; it’s a critical process that protects your business from costly payroll errors, tax compliance issues, and inaccurate financial reporting. By regularly reconciling payroll records with bank transactions, general ledger accounts, and tax filings, businesses can ensure employees are paid accurately, maintain compliance with federal and state regulations, and make informed financial decisions based on reliable data.

As your business grows, payroll becomes increasingly complex. Partnering with experienced professionals can help you streamline payroll processes, reduce compliance risks, and free up valuable time to focus on growing your business.

Ready to simplify payroll reconciliation and strengthen your financial operations? Schedule a free consultation with Veemi Accounting today and discover how our outsourced payroll, bookkeeping, and accounting solutions can support your business.

FAQs

Payroll reconciliation should ideally be completed after every payroll cycle, whether payroll is processed weekly, bi-weekly, semi-monthly, or monthly. Reconciling regularly helps identify discrepancies before quarterly tax filings and year-end reporting, reducing the risk of compliance issues and costly corrections.

A complete payroll reconciliation typically requires the payroll register, employee earnings reports, general ledger entries, payroll clearing account records, bank statements, payroll tax reports (such as Forms 941 and 940), benefit deduction reports, retirement contribution records, and payroll software summaries. Keeping these documents organized makes it easier to identify and resolve discrepancies.

Yes. Regular payroll reconciliation creates a clear audit trail by documenting payroll calculations, tax deposits, employee deductions, and accounting entries. If your business is selected for an IRS payroll audit, well-maintained reconciliation records can help demonstrate compliance, support reported figures, and reduce the time required to respond to audit requests.

Multi-state employers must comply with different state income tax rules, unemployment insurance requirements, local payroll taxes, and filing deadlines. Payroll reconciliation helps verify that taxes have been withheld and reported correctly for each employee’s work location, reducing the risk of state-level penalties and reporting errors